A plain-English guide for litigants in person

You have been wronged. You know it. Your opponent knows it. The judge probably suspects it. And then the judgment comes back against you — not because the wrong didn’t happen, but because you couldn’t connect it to the harm you suffered.

Causation is where many well-founded civil claims die. Not on the facts. Not on the law. On the invisible chain of logic that runs from what the defendant did to what happened to you. Courts do not ask “did the defendant behave badly?” as a standalone question. They ask “did the defendant’s bad behaviour cause this particular damage?” Those are very different questions, and failing to understand the difference is one of the most common ways litigants in person lose cases they should win.

This article explains causation in civil claims in plain English. It covers the but-for test, what happens when but-for doesn’t work cleanly, remoteness of damage, the thin skull rule, the novus actus interveniens doctrine, intervening decisions by the claimant and third parties, and the duty to mitigate. You will not need a law degree to follow it. You will need to read carefully.

Start here: what causation actually means

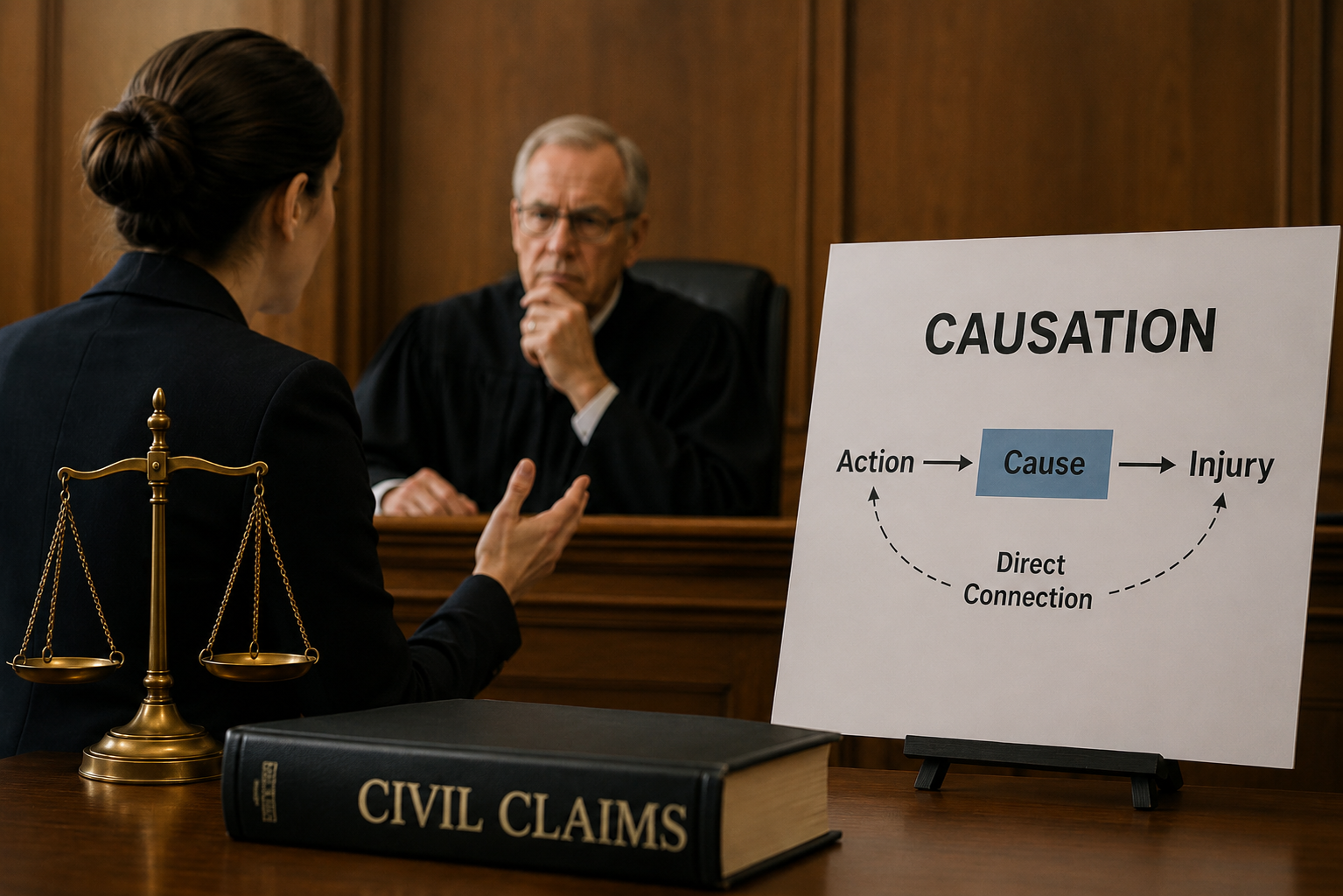

Causation in civil law is the legal mechanism that links a defendant’s wrongful act or omission to the claimant’s loss. Proving that the defendant was negligent, or in breach of contract, or committed a tort, is only the first half of a civil claim. The second half is proving that the breach caused the damage you are claiming for.

These two things — breach and causation — are completely separate exercises. A defendant can be in clear, undeniable breach and yet escape liability if the claimant cannot establish that the breach caused the claimed harm. This is not a technicality. It is a logical principle: a wrongdoer should only be held responsible for the consequences that actually flowed from the wrong they committed.

Causation in civil law has two distinct layers. The first is factual causation — did the defendant’s act actually bring about the harm? The second is legal causation — even if factually linked, is the harm the kind of thing the law holds the defendant responsible for? Get either layer wrong and the claim fails.

The but-for test — the starting point for every causation argument

The primary tool for factual causation is the but-for test. It asks a single question: but for the defendant’s breach, would the claimant’s loss have occurred?

If the answer is no — the loss would not have happened without the breach — causation is established. If the answer is yes — the loss would have happened anyway, with or without the breach — causation fails and the claim fails with it.

The most famous illustration is Barnett v Chelsea & Kensington Hospital Management Committee [1969] 1 QB 428. A hospital nurse sent away a man who arrived complaining of illness after drinking tea. He died five hours later of arsenic poisoning. The hospital was clearly in breach of its duty of care. But the evidence showed that the arsenic dose he had ingested was so large that even if he had been immediately admitted and treated, he would have died anyway. The but-for test failed. The breach did not cause the death. The claim failed.

For litigants in person, this is a cold and uncomfortable principle. It means that being able to show the defendant did something wrong is not enough. You must be able to say: and if they hadn’t done that wrong thing, I would not have suffered this loss. Ask yourself this question before issuing: if the defendant had behaved perfectly, would I still have ended up where I am now? If the honest answer is probably yes, you have a causation problem.

Examples from the kinds of disputes LiPs commonly bring:

You claim your landlord’s failure to fix damp made you ill. But medical evidence shows your respiratory condition pre-dates the damp and is attributable to something else entirely. But-for fails — the illness existed independently of the breach.

You claim a neighbour’s trespass onto your garden destroyed your plants. But a photograph from the same week shows the plants were already dead before the trespass occurred. But-for fails.

You claim a solicitor gave you negligent advice on a settlement and you lost money as a result. But the evidence shows you would have accepted the same settlement regardless of the advice, because you had no appetite for a trial. But-for fails.

The key discipline is to be honest with yourself before the claim reaches a courtroom, because the defendant’s advocate will ask these questions with considerably less sympathy.

When but-for doesn’t work cleanly — material contribution

The but-for test assumes a world of clean, single causes. Reality is messier. In some cases, the damage has multiple potential causes, and it is scientifically or factually impossible to say which cause actually did the damage. Courts have developed modified approaches for these situations.

The foundational case is Bonnington Castings Ltd v Wardlaw [1956] AC 613. A steel-dresser developed pneumoconiosis from inhaling silica dust at work. Some of the dust came from sources the employer could not have prevented (innocent dust). Some came from sources caused by the employer’s breach of safety regulations (guilty dust). Medical evidence could not say which individual dust particles had actually caused the disease. The House of Lords held that liability was established if the employer’s breach had materially contributed to the disease — that is, made a real and substantial contribution to it. A negligible contribution would not suffice, but a genuine contribution, even if not the sole or dominant cause, was enough.

McGhee v National Coal Board [1973] 1 WLR 1 went further. A worker developed dermatitis from brick dust. The employer was not responsible for exposure during working hours, but was responsible for failing to provide washing facilities, so workers had to cycle home caked in dust, extending exposure. Medical science could not say whether the disease was caused by the working-time exposure or the cycling-home exposure. The House of Lords held that materially contributing to the risk of the disease was sufficient for liability.

The practical message for LiPs: if you cannot establish but-for causation because there are multiple potential causes and you cannot isolate the defendant’s contribution, consider whether you can argue material contribution instead. This requires showing that the defendant’s breach made a real, more-than-negligible contribution to either the damage itself or the risk of the damage occurring. It is a lower bar than but-for, but courts will not allow speculation or bare assertion to substitute for evidence.

Remoteness — the harm must be a foreseeable type

Factual causation is only the first layer. Even where the defendant’s breach factually caused the damage, a second legal question arises: was the harm too remote to be recoverable?

The modern test for remoteness comes from Overseas Tankship (UK) Ltd v Morts Dock and Engineering Co Ltd [1961] AC 388, universally called The Wagon Mound (No 1). A ship negligently spilled furnace oil into Sydney Harbour. The oil floated to a wharf where welding was in progress. Molten metal fell on the oil, which caught fire, and the wharf burned down. The Privy Council held the ship-owner was not liable for the fire damage. Although the spill was negligent, and although it factually caused the fire, the fire damage was not recoverable because fire damage was not a reasonably foreseeable consequence of an oil spill of this type. The rule established: a defendant is liable only for harm of a type that was reasonably foreseeable at the time of the breach.

Not the exact manner of the harm. Not the precise extent of it. The type.

Hughes v Lord Advocate [1963] AC 837 illustrates this. Post-office workers left a manhole open, guarded only by paraffin lamps. A child picked up a lamp, dropped it into the manhole, and an explosion followed — caused by the paraffin vapour behaving in an unusual way that experts would not have predicted. The House of Lords found liability. The type of harm — burning — was foreseeable. That the specific mechanism was unusual did not take the harm outside the foreseeable type.

For LiPs, the remoteness question is essentially this: stand back from what actually happened, and ask whether a reasonable person in the defendant’s position, at the time of the breach, would have recognised that some harm of this general kind was a real possibility. If yes, the type of harm is recoverable even if the exact way it materialised was unusual. If no — if what happened to you was something wholly outside any foreseeable consequence of the defendant’s conduct — the claim for that head of loss may fail at the remoteness stage.

A defendant landlord fails to fix a faulty boiler, knowing the boiler is dangerous. You suffer carbon monoxide poisoning. Physical harm from a dangerous boiler was foreseeable — recoverable.

A contractor negligently leaves scaffolding unsecured. An unusually severe storm hurls it into a parked car. Whether recoverable turns on whether property damage from unsecured scaffolding was foreseeable — and the answer is almost certainly yes, because preventing that exact thing is the whole point of securing scaffolding. The unusual weather does not make the type of damage unforeseeable.

The thin skull rule — take your victim as you find them

Remoteness and the thin skull rule pull in opposite directions, and the interaction between them is one of the most misunderstood areas of causation law.

The remoteness rule says: you only recover for foreseeable types of harm.

The thin skull rule says: once the type of harm is foreseeable, you are liable for the full extent of that harm, even if the claimant’s particular vulnerability meant the harm was far worse than it would have been for an ordinary person.

The leading case is Smith v Leech Brain & Co Ltd [1962] 2 QB 405. A worker was burned on his lip by a splash of molten metal — a foreseeable type of harm from the work being done. Unknown to anyone, his lip tissue had a pre-malignant condition. The burn triggered cancer and the worker died. The defendant argued that the fatal cancer was not foreseeable and was too remote. The court rejected that argument. The type of harm — a burn — was foreseeable. The defendant had to take the claimant as he found him, including the pre-malignant condition that made an ordinary burn fatal.

The principle for LiPs: if you have a pre-existing physical or psychiatric condition that makes you more vulnerable to harm, and a foreseeable type of harm is made catastrophically worse because of that vulnerability, the defendant cannot hide behind the vulnerability to reduce what they owe you. They took the risk of the full consequences when they breached their duty.

This is particularly significant in police litigation. A claimant who develops serious PTSD from an unlawful arrest — because they had pre-existing mental health vulnerabilities — can recover for the full psychiatric damage, not merely what would have been suffered by a person without those vulnerabilities, provided the type of harm (some psychological impact) was foreseeable from an unlawful arrest.

The key distinction: the thin skull rule does not override remoteness entirely. The type of harm must still be foreseeable. What the rule prevents is the defendant arguing that the unusual severity of the harm, caused by the claimant’s particular vulnerability, takes the claim outside recovery. Foreseeable type: yes. Unexpectedly severe extent: covered.

Novus actus interveniens — when something breaks the chain

The Latin phrase means new intervening act. It describes a situation where, after the defendant’s breach, a further event occurs that is sufficiently independent and sufficiently significant that it breaks the causal chain between the breach and the claimant’s loss. If a novus actus is established, the defendant’s breach ceases to be a legal cause of the loss.

Third-party acts

The leading example of a third-party novus actus is Home Office v Dorset Yacht Co Ltd [1970] AC 1004. Borstal trainees under supervision escaped and damaged a yacht. The House of Lords held the Home Office liable because it was reasonably foreseeable that inadequately supervised borstal boys would escape and cause damage to nearby property. The deliberate acts of the boys did not break the chain because those very acts were precisely what the duty of supervision was designed to prevent.

Compare Lamb v Camden London Borough Council [1981] QB 625. The council negligently broke a water main, which caused the claimant’s house to be temporarily vacated. During the vacancy, squatters moved in and caused extensive damage. The Court of Appeal held the council was not liable for the squatters’ damage. The squatters’ deliberate criminal trespass was not sufficiently foreseeable as a consequence of a burst water main to extend the chain of causation.

The principle: a deliberate wrongful act by a third party is more likely to break the chain than an accidental act. But not always — if the very purpose of the defendant’s duty was to guard against that type of third-party intervention, the chain is not broken. Stansbie v Troman [1948] 2 KB 48 confirms this: a decorator left a house unlocked while on an errand; a thief entered and stole valuables; the decorator was held liable. The whole point of the implied obligation not to leave the house unsecured was to prevent exactly that kind of loss. The thief’s deliberate act did not break the chain.

For LiPs: the test is whether the intervening act was a foreseeable consequence of the defendant’s breach, or whether it was something truly independent and outside the scope of the risk created by the breach. If the third party’s act was something the defendant should have guarded against, the chain is intact. If the intervening act was genuinely unconnected and unforeseeable, the chain breaks and the defendant’s liability ends at that point.

The claimant’s own intervening act

A claimant’s own act can also break the chain — but the threshold is high, and the outcome can differ between a complete break (novus actus, claim fails for the later harm) and contributory negligence (claim succeeds but damages are reduced).

McKew v Holland & Hannen & Cubitts (Scotland) Ltd [1969] 3 All ER 1621 is the paradigm case. The claimant had suffered a leg injury due to the defendant’s negligence, leaving his leg prone to giving way. Knowing this, he chose to descend a steep staircase without a handrail while carrying a child. His leg gave way, he jumped to avoid falling on the child, and fractured his ankle badly. The House of Lords held that the claimant’s own unreasonable act — attempting a steep staircase in that condition without taking precautions — was a novus actus. The chain between the original leg injury and the ankle fracture was broken.

The test is unreasonableness. If the claimant’s own conduct in response to the defendant’s breach was so unreasonable that no ordinary person would have done it, and it caused further injury, that further injury falls outside the defendant’s liability. If the claimant’s response, while perhaps imprudent, was within the range of normal human reaction to the situation the defendant created, the chain is not broken — contributory negligence may reduce the damages, but it does not defeat the claim.

This distinction matters enormously. If you suffered harm from a defendant’s conduct and then made a subsequent decision that arguably worsened your position, the question is whether your decision was genuinely unreasonable — something no reasonable person in your situation would have done — or whether it was understandable human behaviour in a difficult situation not of your making. The latter attracts a finding of contributory negligence and a percentage reduction in damages. The former risks the court finding a novus actus that severs the claim for the later harm entirely.

Contributory negligence — sharing the blame

Where the claimant’s own conduct contributed to the harm but did not rise to the level of a novus actus, the court will typically apply the Law Reform (Contributory Negligence) Act 1945. The court assesses the claimant’s share of responsibility and reduces the damages proportionately.

Froom v Butcher [1976] QB 286 established the approach in the road accident context — a passenger who did not wear a seatbelt had their damages reduced by 25% where wearing one would have prevented the injury entirely, and by 15% where it would have reduced the injury. The principle applies wherever the claimant’s conduct fell below the standard of a reasonable person taking care of their own safety or interests.

The critical message for LiPs: contributory negligence reduces your recovery, it does not defeat it. If you can show the defendant was primarily responsible for the harm, you recover a reduced figure. That is a very different — and much better — outcome than a finding that your own act broke the chain entirely.

Mitigation — you cannot just sit back

Even where causation is fully established, the law imposes a duty on the claimant to take reasonable steps to mitigate their loss. You cannot recover for losses you could have avoided with reasonable effort.

The duty does not require extraordinary steps or unreasonable expense. It requires reasonable conduct in response to the damage the defendant has caused. The burden of proving a failure to mitigate lies on the defendant — it is for the defendant to show that the claimant took unreasonable steps, or failed to take reasonable ones.

Payzu Ltd v Saunders [1919] 2 KB 581 established that a claimant must accept a reasonable alternative offer from the defendant if refusing it would unnecessarily increase their loss. A claimant who refuses a genuine, reasonable offer in order to run up a larger damages claim will find their recovery limited to what it would have been had they accepted the offer.

In personal injury and police misconduct claims, mitigation issues most commonly arise around medical treatment and employment. A claimant who refuses reasonable treatment or rehabilitation cannot recover for losses that treatment would have reduced. A claimant who has lost income due to injury is expected to seek alternative work within their capacity.

The important limits: the standard is reasonableness, assessed in context. You are not expected to undergo painful or risky treatment, accept humiliating employment, or accept inadequate settlement offers. What you are expected to do is behave as a reasonable person in your situation — take sensible steps to help yourself where you genuinely can, rather than treating the defendant as an underwriter of unlimited loss.

Scope of duty — a limit on causation that professionals will raise

One further principle deserves attention. Since South Australia Asset Management Corporation v York Montague Ltd [1997] AC 191 — universally cited as SAAMCO — where a defendant assumed responsibility only for providing specific information or advice, their liability is confined to the consequences of that information being wrong. It does not extend to the full range of losses suffered by the claimant, even where those losses were factually caused by reliance on the advice.

In that case, valuers gave over-valuations of properties. Lenders relied on the valuations and advanced loans. When the property market fell, the losses were far greater than simply the amount of over-valuation. The valuers were held liable only for the amount by which the valuations were wrong — not for market-fall losses, which were a risk the lenders had independently assumed.

The SAAMCO principle operates as a cap on causation: even where but-for and foreseeability are both satisfied, the defendant’s liability is confined to the scope of the duty they actually assumed. This matters most in professional negligence cases and in claims where consequential losses go significantly beyond the specific risk the defendant was responsible for managing. If you are claiming against a professional — a solicitor, surveyor, accountant, or similar — expect this argument.

Pulling it together — a causation checklist

When building or evaluating a civil claim, work through these questions for each head of damage separately. Causation is not a single all-or-nothing exercise; it is assessed loss by loss.

First, identify the specific loss claimed. Second, apply the but-for test: but for the defendant’s breach, would this loss have occurred? If no, causation is established. If yes, consider material contribution. Third, if but-for is problematic because of multiple concurrent causes, consider whether the defendant’s breach made a real and more-than-negligible contribution. Fourth, check remoteness: was the type of harm suffered a reasonably foreseeable consequence of this kind of breach? Fifth, if you have a pre-existing vulnerability that amplified the harm, apply the thin skull rule — the defendant takes you as they find you once the type of harm is foreseeable. Sixth, consider whether any later act — by you or a third party — was so independent and unreasonable that it severed the causal link. Seventh, identify any losses you could have mitigated by reasonable steps and be prepared to address them. Eighth, in cases against professionals, consider whether the SAAMCO principle caps the defendant’s liability to the specific risk they were responsible for managing.

None of these questions has a mechanical answer. Causation in civil law is ultimately a normative exercise — courts are asking what it is fair and reasonable to hold this defendant responsible for. The law gives structure to that inquiry, but it cannot eliminate judgment. What it can do is tell you which arguments to make, which evidence to gather, and which of your claimed losses stand the best chance of surviving scrutiny at trial.

This article is a general commentary for informational purposes; it is not legal advice and does not create a solicitor-client relationship. Get professional legal advice for your specific situation.